Potential Upside For Sipai Health Technology Co., Ltd. (HKG:314) Not Without Risk

Not Without Risk")

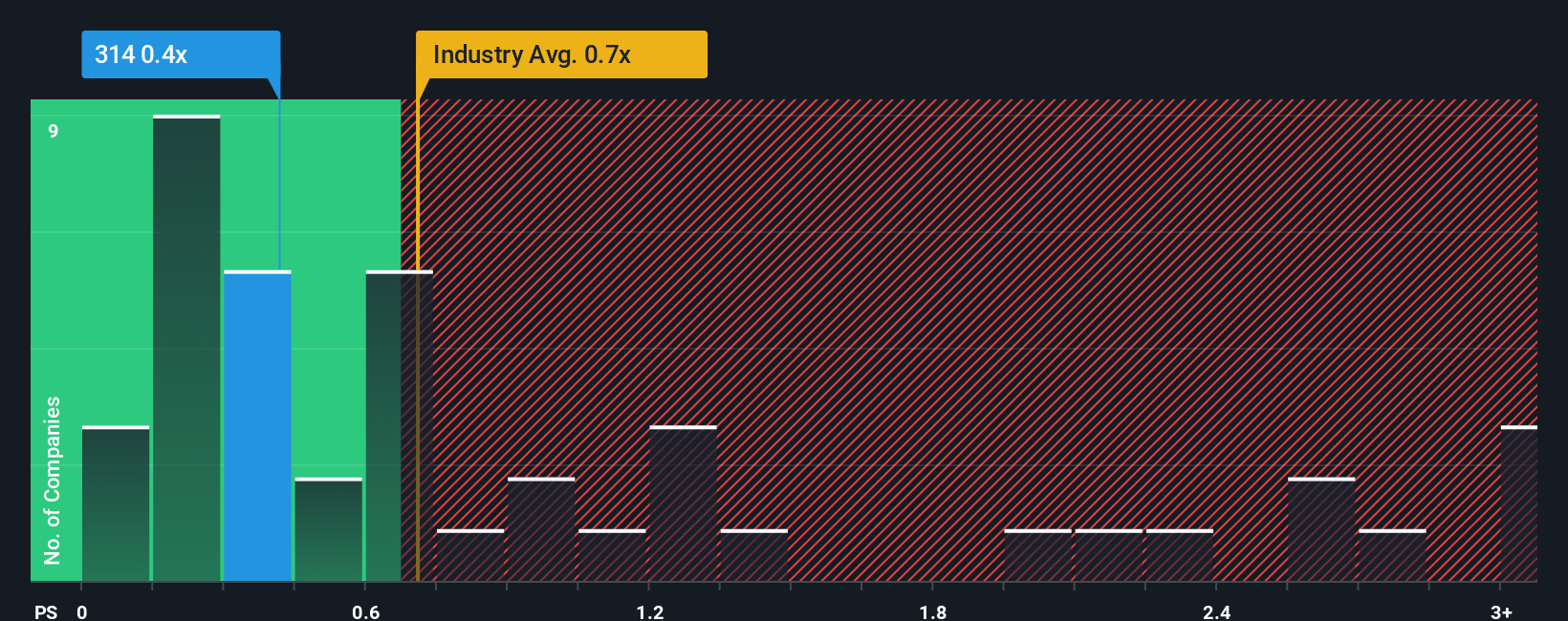

It’s not a stretch to say that Sipai Health Technology Co., Ltd.’s (HKG:314) price-to-sales (or “P/S”) ratio of 0.4x right now seems quite “middle-of-the-road” for companies in the Consumer Retailing industry in Hong Kong, where the median P/S ratio is around 0.7x. Although, it’s not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

AI is about to change healthcare. These 20 stocks are working on everything from early diagnostics to drug discovery. The best part – they are all under $10bn in marketcap – there is still time to get in early.

See our latest analysis for Sipai Health Technology

What Does Sipai Health Technology’s Recent Performance Look Like?

Sipai Health Technology could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. It might be that many expect the dour revenue performance to strengthen positively, which has kept the P/S from falling. If not, then existing shareholders may be a little nervous about the viability of the share price.

If you’d like to see what analysts are forecasting going forward, you should check out our free report on Sipai Health Technology.

Do Revenue Forecasts Match The P/S Ratio?

There’s an inherent assumption that a company should be matching the industry for P/S ratios like Sipai Health Technology’s to be considered reasonable.

Retrospectively, the last year delivered a frustrating 26% decrease to the company’s top line. This means it has also seen a slide in revenue over the longer-term as revenue is down 10% in total over the last three years. Therefore, it’s fair to say the revenue growth recently has been undesirable for the company.

Turning to the outlook, the next year should generate growth of 49% as estimated by the lone analyst watching the company. With the industry only predicted to deliver 20%, the company is positioned for a stronger revenue result.

In light of this, it’s curious that Sipai Health Technology’s P/S sits in line with the majority of other companies. It may be that most investors aren’t convinced the company can achieve future growth expectations.

The Final Word

Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Looking at Sipai Health Technology’s analyst forecasts revealed that its superior revenue outlook isn’t giving the boost to its P/S that we would’ve expected. Perhaps uncertainty in the revenue forecasts are what’s keeping the P/S ratio consistent with the rest of the industry. At least the risk of a price drop looks to be subdued, but investors seem to think future revenue could see some volatility.

Plus, you should also learn about this 1 warning sign we’ve spotted with Sipai Health Technology.

It’s important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Try a Demo Portfolio for Free

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

link